Roth IRA Contribution Limits 2024 are here, and understanding these changes is crucial for maximizing retirement savings. This year brings adjustments to contribution limits, income restrictions, and spousal contribution rules, impacting how much individuals can contribute to their Roth IRAs. Navigating these updated guidelines is key to securing your financial future.

This article provides a comprehensive guide to the 2024 Roth IRA contribution limits, including detailed explanations of income limitations, spousal contribution rules, and catch-up contributions for those age 50 and older. We’ll also explore the tax implications of Roth IRA contributions and offer strategies for maximizing your contributions.

Roth IRA Contribution Limits 2024

The 2024 Roth IRA contribution limits represent a significant aspect of retirement planning for many Americans. Understanding these limits, along with associated income restrictions and spousal contribution rules, is crucial for maximizing retirement savings and minimizing potential tax liabilities. This article provides a comprehensive overview of the 2024 Roth IRA contribution rules, offering insights into contribution limits, income restrictions, spousal contributions, catch-up contributions, tax implications, and strategic planning.

Roth IRA Contribution Limits for 2024, Roth Ira Contribution Limits 2024

The contribution limits for Roth IRAs in 2024 have been adjusted to reflect inflation. For individuals under age 50, the maximum contribution remains unchanged from 2023. However, those age 50 and older benefit from an increased catch-up contribution.

Exceeding the contribution limit can result in significant penalties. The IRS imposes a 6% tax on the excess contribution, payable annually until the excess is corrected. This penalty can substantially impact your retirement savings.

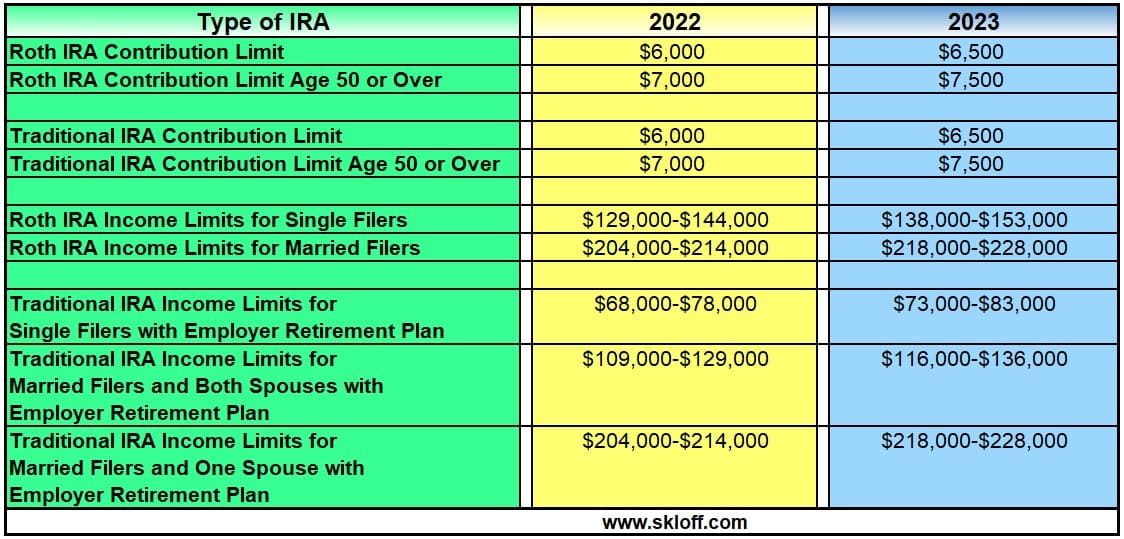

| Contribution Limit | 2023 | 2024 |

|---|---|---|

| Individuals Under 50 | $6,500 | $6,500 |

| Individuals Age 50 and Older | $7,500 | $7,500 |

Income Limits and Roth IRA Eligibility

Eligibility for Roth IRA contributions is subject to modified adjusted gross income (MAGI) limits. These limits determine whether you can make a full contribution, a partial contribution, or no contribution at all. Exceeding the income limits doesn’t necessarily disqualify you entirely, but it may reduce your contribution amount or prevent you from contributing altogether.

- Single Filers: Full contribution allowed up to a certain MAGI. Partial contributions may be allowed within a higher MAGI bracket. No contribution allowed above a specified MAGI threshold. (Specific MAGI thresholds for 2024 need to be verified from official IRS sources.)

- Married Filing Jointly: Similar to single filers, full, partial, or no contributions are determined by MAGI brackets. (Specific MAGI thresholds for 2024 need to be verified from official IRS sources.)

Spousal IRA Contributions

In 2024, if both spouses are eligible to contribute to a Roth IRA, each can contribute the maximum amount, regardless of the other spouse’s income. Even if one spouse earns significantly more than the other, both can still contribute up to the individual limits. For example, if one spouse earns $200,000 and the other earns $10,000, both can contribute the maximum allowed for their age group, provided they meet the individual MAGI limits.

The higher earner’s income does not affect the lower earner’s ability to contribute.

Catch-Up Contributions for those age 50 and Older

Source: skloff.com

With the 2024 Roth IRA contribution limits recently announced, many are focusing on maximizing their retirement savings. However, financial planning isn’t the only thing on people’s minds; some may also be checking local classifieds, such as craigslist jackson michigan personals , for other opportunities. Ultimately, responsible financial planning, including understanding Roth IRA limits, remains crucial for long-term security.

Individuals age 50 and older in 2024 can make an additional catch-up contribution. This allows them to contribute more to their Roth IRA to help accelerate their retirement savings.

For example, a 55-year-old can contribute $6,500 (regular contribution) + $1,000 (catch-up contribution) = $7,500.

Catch-up contributions offer a significant advantage, providing an extra boost to retirement savings during the later years of one’s working life. This can help bridge the gap between current savings and desired retirement income.

Tax Implications of Roth IRA Contributions

Roth IRA contributions are made with after-tax dollars. This means you pay income taxes on the money before it goes into the IRA. However, qualified withdrawals in retirement are tax-free. This contrasts with traditional IRAs, where contributions are tax-deductible, but withdrawals are taxed in retirement. High-income earners may find that the tax benefits of Roth IRAs are less pronounced, as they are already in higher tax brackets.

For example, a $6,500 contribution to a Roth IRA means you pay taxes on that $6,500 now. In contrast, a $6,500 contribution to a traditional IRA allows you to deduct that amount from your taxable income this year, but you’ll pay taxes on it in retirement. The best choice depends on individual circumstances and predictions about future tax rates.

Contribution Strategies and Planning

Maximizing Roth IRA contributions requires careful planning and consideration of income limits. Individuals approaching retirement age should prioritize maximizing their contributions to the extent possible, given their income and other financial obligations. Consistent contributions over time offer the most significant long-term benefits through compounding returns.

A step-by-step approach might involve: 1) determining eligibility based on income; 2) calculating the maximum contribution; 3) setting up automatic contributions; 4) reviewing contributions annually; 5) adjusting strategy as needed.

Illustrative Example: A Couple’s Contribution Strategy

Consider a married couple, Sarah (age 48, earning $80,000) and John (age 52, earning $120,000). Both are eligible to contribute to Roth IRAs. Sarah can contribute $6,500. John can contribute $6,500 + $1,000 (catch-up) = $7,500. Their combined contributions total $14,000.

They have maximized their contributions while staying within the limits, ensuring tax-free withdrawals in retirement.

- Sarah: Age 48, Income $80,000, Contribution $6,500

- John: Age 52, Income $120,000, Contribution $7,500

- Total Contribution: $14,000

Closure: Roth Ira Contribution Limits 2024

Planning for retirement requires careful consideration of various factors, and understanding the nuances of Roth IRA contribution limits is paramount. By staying informed about these annual adjustments and employing effective contribution strategies, individuals can significantly enhance their retirement savings. Remember to consult with a financial advisor for personalized guidance tailored to your specific financial situation.